How Extra Mortgage Payments Reduce Your Loan: The Math Explained

Extra mortgage payments go directly to principal, cutting future interest charges. Learn the math behind one extra payment per year, bi-weekly payments, and lump sums.

- extra mortgage payments

- pay off mortgage faster

- mortgage payoff calculator

- bi-weekly mortgage

- mortgage principal

This article is for educational purposes only. It does not constitute financial or legal advice. Consult a licensed financial professional or HUD-approved housing counselor before making mortgage decisions.

Every dollar you pay toward your mortgage principal is a dollar that will never generate another interest charge. Because mortgage amortization is front-loaded with interest, extra payments made in the early years of a loan are among the most leveraged financial moves available to a homeowner.

This article walks through the math behind three common extra-payment strategies: one extra payment per year, bi-weekly payments, and lump-sum prepayments. All figures are illustrative examples and not a representation of current market rates.

Why Extra Payments Are So Powerful

Recall the fundamental rule of mortgage interest:

Monthly Interest = Outstanding Balance × (Annual Rate ÷ 12)

When you make an extra principal payment, the balance falls. Every future month’s interest is then calculated on a smaller number. That lower balance compounds forward — each month that you owe less is a month that generates less interest, which in turn leaves more of your regular payment available for principal, which brings the balance down faster. It is a self-reinforcing cycle.

The earlier in the loan’s life that you reduce the balance, the longer this compounding effect works in your favor.

Strategy 1: One Extra Payment Per Year

The simplest extra-payment strategy is making one additional full payment each year. This can be done as a single lump sum (often using a year-end bonus or tax refund) or by dividing it into monthly increments of 1/12 of your payment.

Example loan: $300,000, 7.0% fixed rate, 30-year term

- Regular monthly payment: $1,995.91

- Total payments (standard): 360

- Total interest paid (standard): ~$418,527

Note: 7.0% used as an illustrative example. Actual rates vary.

With one extra full payment per year:

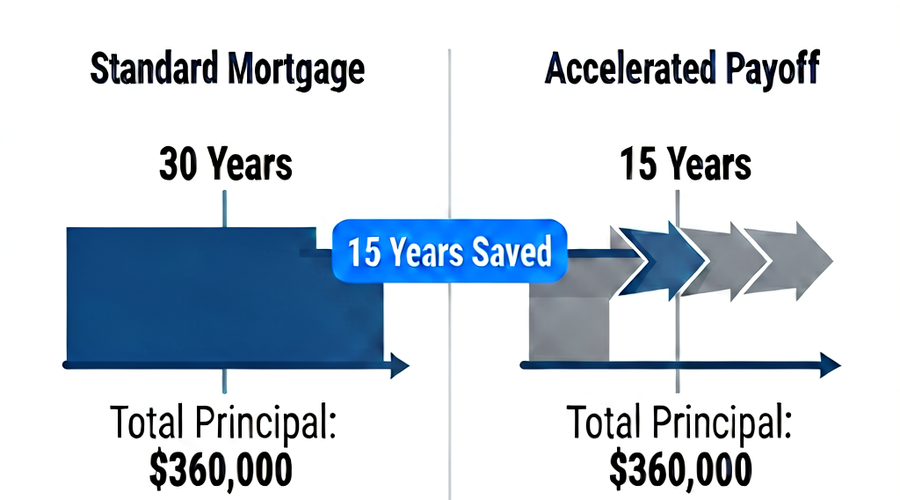

- Loan pays off approximately 4.5 years early (around Month 306)

- Total interest paid: approximately $363,000

- Interest saved: approximately $55,000+

The math works because each extra payment is applied entirely to principal, causing every subsequent payment to carry a slightly smaller interest charge. The effect compounds over decades.

Strategy 2: Bi-Weekly Payments

A bi-weekly payment plan means paying half your monthly mortgage payment every two weeks instead of one full payment per month. This is not simply paying the same amount on a different schedule — it produces an extra full payment each year through calendar arithmetic.

Why: There are 52 weeks in a year, which means 26 bi-weekly periods, which equals 13 full monthly payments rather than 12.

Same $300,000, 7.0%, 30-year loan under bi-weekly payment:

- Bi-weekly payment: $997.96 (half the monthly amount)

- Annual total paid: $997.96 × 26 = $25,946.96 vs. $23,950.92 standard

- Loan pays off approximately 4–5 years early

- Interest savings: approximately $50,000–$60,000

Figures are approximate and will vary by loan specifics.

Important caveats:

- Verify your loan servicer actually applies bi-weekly payments as received, rather than holding them until the end of the month. Some servicers require enrollment in a formal bi-weekly program.

- Some servicers charge a setup fee for bi-weekly programs. Evaluate whether the interest savings justify the fee — they almost always do for early-term loans.

- You can replicate the exact same benefit by simply adding 1/12 of your monthly payment to each regular monthly payment and designating it as principal-only.

The CFPB recommends confirming with your servicer how extra payments are applied before assuming the benefit will be realized. (CFPB — How can I pay off my mortgage sooner?)

Strategy 3: Lump-Sum Prepayments

A lump-sum prepayment is a one-time extra payment applied entirely to principal — often funded by a bonus, inheritance, home sale proceeds, or tax refund.

Same $300,000, 7.0%, 30-year loan:

| Lump Sum Applied at Month 12 | Payoff Month | Interest Saved |

|---|---|---|

| $5,000 | ~Month 351 | ~$11,000 |

| $10,000 | ~Month 343 | ~$21,000 |

| $20,000 | ~Month 326 | ~$40,000 |

| $50,000 | ~Month 282 | ~$86,000 |

Figures are approximate illustrations. Actual savings depend on exact loan terms.

Notice the non-linear relationship: a $50,000 lump sum does not save exactly 10× what a $5,000 payment saves. It saves more — because the larger principal reduction has more months over which to compound its interest savings.

Timing matters: The earlier in the loan’s life the lump sum is applied, the more interest it saves. A $20,000 payment in Year 1 saves considerably more than the same $20,000 in Year 20, because the Year 1 payment avoids nearly two additional decades of interest accrual.

Monthly Incremental Extra Payments

Adding a fixed extra amount to every monthly payment is the most consistent and predictable approach for borrowers who prefer systematic savings over one-time moves.

Same $300,000, 7.0%, 30-year loan:

| Extra Per Month | Payoff Date | Total Interest | Interest Saved |

|---|---|---|---|

| $0 (baseline) | Month 360 | ~$418,527 | — |

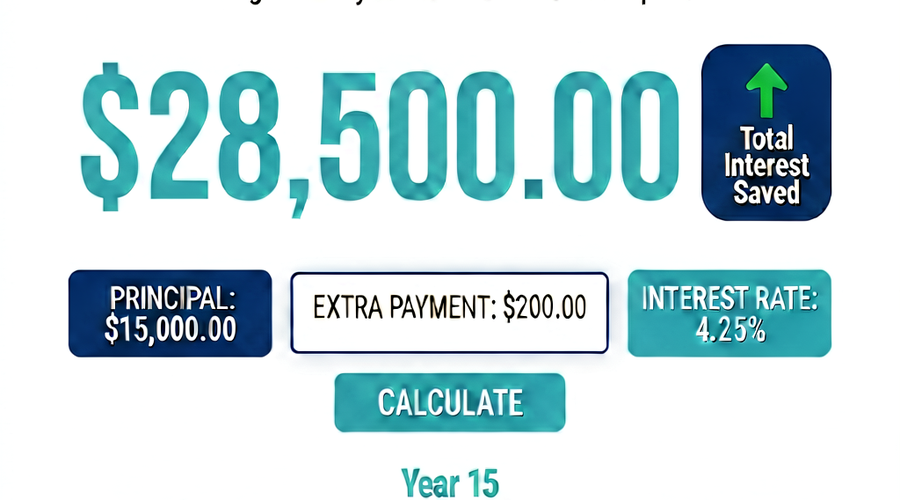

| $100 | ~Month 340 | ~$390,000 | ~$28,500 |

| $200 | ~Month 322 | ~$364,000 | ~$54,500 |

| $500 | ~Month 285 | ~$306,000 | ~$112,500 |

| $1,000 | ~Month 244 | ~$234,000 | ~$184,500 |

Figures are approximate illustrations.

Even $100 per month — less than $1,200 per year — saves approximately $28,500 in interest and cuts nearly two years off a 30-year loan.

Check for Prepayment Penalties First

Before accelerating your mortgage, confirm there is no prepayment penalty. Prepayment penalties were once more common in certain mortgage products; while the Dodd-Frank Act significantly restricted prepayment penalties on most residential mortgages, they can still exist in some circumstances.

Your loan documents will specify whether a prepayment penalty applies. If you cannot locate this information, your mortgage servicer is required to provide it. The CFPB provides guidance on understanding your loan terms and your rights as a borrower. (CFPB — Paying Off a Loan Early)

Ensure Extra Payments Are Applied to Principal

When submitting extra payments, always:

- Label them clearly — write “apply to principal” on a check, or use your servicer’s online portal to designate principal-only payments

- Confirm application — verify on your next statement that the extra amount reduced your principal balance rather than being held in a suspense account

- Keep records — retain confirmation of all extra payments and their application

Some servicers automatically apply any amount above the regular payment to principal; others do not. Do not assume — verify.

Freddie Mac notes that ensuring payments are correctly applied is the borrower’s responsibility, and that misapplied payments can undermine the intended payoff acceleration.

Opportunity Cost: When Extra Payments May Not Be the Best Move

The financial case for extra mortgage payments depends on context. Making extra mortgage payments is most compelling when:

- Your mortgage rate is higher than the expected return on alternative investments (after tax)

- You have already maxed out tax-advantaged accounts (401(k), IRA)

- You have no high-interest debt (credit card debt at 20%+ should be eliminated before making extra mortgage payments)

- You value the security of a paid-off home

The CFPB recommends weighing all of these factors with a qualified financial advisor before committing to accelerated mortgage payoff, since liquidity, retirement savings, and emergency fund needs also play a role in the decision.

Running Your Own Numbers

The examples above use illustrative rates and loan amounts. Your actual savings depend on your specific loan balance, interest rate, remaining term, and the timing and amount of extra payments.

Use our amortization calculator to model any extra-payment scenario against your real loan details. Enter your current balance, rate, and remaining term as the baseline, then add extra payment amounts to see precisely how many months and how many dollars you save.