Interest vs. Principal: Why You Pay So Much Interest at the Start of a Mortgage

In the early years of a mortgage, most of each payment is interest. Understand why this happens, how the split shifts over time, and what it means for your finances.

- interest vs principal

- mortgage interest

- principal and interest

- how mortgage interest works

- amortization front-loaded

This article is for educational purposes only. It does not constitute financial or legal advice. Consult a licensed financial professional or HUD-approved housing counselor before making mortgage decisions. Tax information in this article is for general educational purposes only — consult a qualified tax professional regarding your specific situation.

Most homeowners making their first few mortgage payments experience a jarring realization: after months of payments, their outstanding balance has barely moved. On a $400,000 mortgage, you might pay $2,500 a month and find your balance only dropped by $350. Where did the rest go?

The answer is interest — and understanding exactly why this happens, and when it changes, is one of the most important things you can learn about your mortgage.

The Mechanism: Interest Accrues on the Outstanding Balance

The key principle governing mortgage interest is simple:

Monthly Interest = Outstanding Balance × (Annual Rate ÷ 12)

Your interest charge each month is not calculated on your original loan amount. It is calculated on whatever you currently owe. When you first take out a mortgage, that amount is at its maximum — so your interest charge is at its maximum.

As you pay down the principal month by month, the outstanding balance shrinks. A smaller balance generates a smaller interest charge. Because your total monthly payment is fixed, that freed-up space automatically flows to principal reduction. The principal reduction accelerates — slowly at first, then faster and faster as the balance falls.

This is not a lender conspiracy. It is simple arithmetic.

A Concrete Example: $400,000 at 7.0% Over 30 Years

7.0% is used here as an illustrative example only. Actual mortgage rates vary with market conditions, borrower creditworthiness, loan type, and lender.

Monthly payment: $2,661.21

Month 1:

- Interest: $400,000 × (0.07 ÷ 12) = $400,000 × 0.005833 = $2,333.33

- Principal: $2,661.21 − $2,333.33 = $327.88

- Remaining balance: $399,672.12

In Month 1, $2,333.33 out of $2,661.21 — 87.7% — goes to interest. Only 12.3% reduces the principal.

The first payment pays down less than $328 on a $400,000 balance. It takes approximately 10 years of regular payments to pay off the first $40,000 of principal on this loan.

The Full Shift: Tracking the Interest/Principal Ratio Over 30 Years

| Year | Monthly Interest | Monthly Principal | % Going to Principal | Balance |

|---|---|---|---|---|

| 1 | ~$2,330 | ~$331 | 12.4% | ~$396,000 |

| 5 | ~$2,254 | ~$407 | 15.3% | ~$382,900 |

| 10 | ~$2,132 | ~$529 | 19.9% | ~$361,800 |

| 15 | ~$1,960 | ~$701 | 26.3% | ~$335,000 |

| 20 | ~$1,716 | ~$945 | 35.5% | ~$294,100 |

| 25 | ~$1,360 | ~$1,301 | 48.9% | ~$233,200 |

| 29 | ~$502 | ~$2,159 | 81.1% | ~$85,900 |

| 30 | ~$16 | ~$2,645 | 99.4% | ~$0 |

Figures are approximate and rounded for illustration.

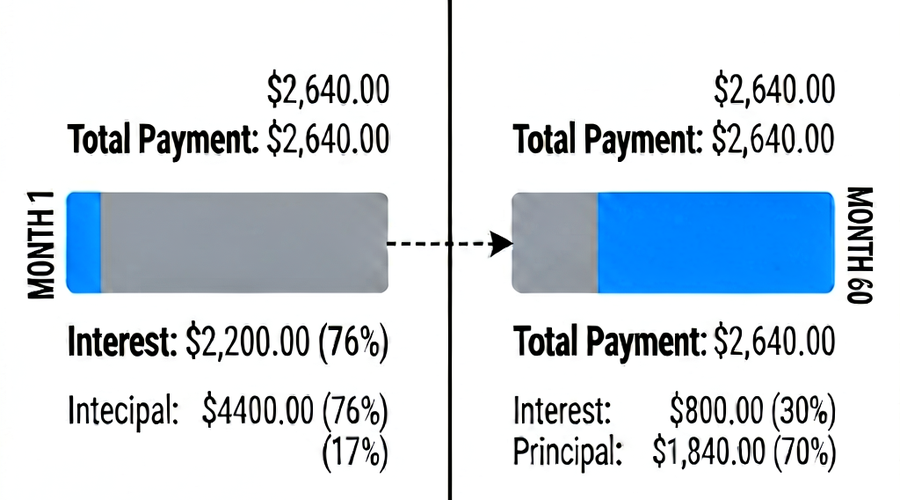

The crossover point — where principal first exceeds interest within a single payment — occurs around Month 253 (roughly Year 21). Before that point, interest takes the majority of every payment. After it, principal takes the majority.

Visualizing the Shift

Imagine a pie chart for your monthly payment. In Year 1, the interest slice is nearly 88%. By Year 10, interest is about 80%. By Year 20, interest has fallen to roughly 64%. By Year 25, interest and principal are nearly equal. In Year 30, interest is a sliver.

This gradual shift is why mortgages behave the way they do: small balance reductions early, accelerating paydown later.

Total Interest Over the Life of the Loan

For the $400,000, 7.0%, 30-year mortgage:

- Total payments: $2,661.21 × 360 = $957,935.60

- Total principal repaid: $400,000

- Total interest paid: ~$557,935

A borrower who takes out a $400,000 mortgage at 7.0% pays well over half a million dollars in interest over 30 years — more than the home itself cost to finance.

This figure alone explains why:

- Making extra principal payments early produces large savings

- Choosing a shorter loan term dramatically reduces total cost

- Refinancing to a lower rate (when appropriate) can save significant money

The Tax Dimension of Mortgage Interest

For some borrowers, a portion of mortgage interest paid may be deductible as an itemized deduction on federal income taxes, subject to eligibility requirements and current tax law.

The IRS Publication 936 governs the home mortgage interest deduction. Key points as of the current publication:

- Interest is deductible on up to $750,000 of mortgage debt (for loans originated after December 15, 2017) for primary and secondary residences

- The standard deduction must be compared to itemized deductions to determine which is beneficial

- Points paid at origination may be deductible in the year paid for a home purchase

Consult a qualified tax professional for advice on your specific tax situation. (IRS Publication 936)

The fact that early mortgage payments carry more interest — and thus potentially more deductible interest — is a consideration some financial planners factor into mortgage payoff strategy. However, tax rules change, and the decision to accelerate or slow paydown should never rest on tax assumptions alone.

Why the Front-Loading Exists: The Financial Logic

Some borrowers feel the front-loaded interest structure is unfair. It is not — it is the mathematically correct way to price a loan.

Consider the lender’s position: on Day 1, they have extended $400,000 that you have not yet paid back. That $400,000 is at risk for the full year (or month, or decade) it remains outstanding. It is rational and correct to charge interest on the amount actually outstanding, not on some future lower balance.

If lenders charged a flat dollar amount of interest regardless of outstanding balance, they would be under-compensated in early months (when their risk is highest) and over-compensated in later months (when the balance is nearly retired). The amortization structure correctly matches interest charges to outstanding risk.

The Federal Reserve has studied the distributional effects of the mortgage interest structure extensively, finding that it is a necessary feature of fixed-payment installment lending and not an arbitrary choice by lenders.

What This Means Practically

1. Extra payments in Year 1 save far more than in Year 25. When the balance is $399,000, an extra $1,000 payment avoids 29 years of interest accrual on that $1,000. At 7%, that $1,000 would generate approximately $1,940 in cumulative interest over 29 years. The same $1,000 in Year 25, with 5 years remaining, avoids about $175.

2. You build equity slowly at first. In the first five years of a 30-year mortgage, you typically pay down only about 4–5% of your original loan balance through regular payments. This is why homeowners who bought with a small down payment and sell early may have little equity despite years of payments — especially if home values have not appreciated.

3. Refinancing resets the clock. When you refinance, you take out a new loan. The amortization schedule starts fresh. If you are 10 years into a 30-year mortgage and refinance into a new 30-year mortgage, you begin again with front-loaded interest — which can mean paying more total interest even if your rate is lower. This trade-off must be carefully evaluated.

4. Understand your real paydown rate before selling. If you need to know how much equity you have, look at your current outstanding balance from your amortization schedule or servicer statement — not the original loan amount minus your down payment. After 5 years of regular payments, you have repaid far less principal than most borrowers expect.

Seeing Your Own Numbers

The examples in this article are illustrative. Your actual interest/principal split depends on your specific loan amount, interest rate, term, and payment history.

Use our amortization calculator to generate a complete, month-by-month breakdown for your loan. Enter your current balance, rate, and remaining term to see exactly how each future payment will be divided — and to model how extra payments would shift that breakdown in your favor.