How Mortgage Amortization Works: Principal, Interest, and Your Monthly Payment

Discover the mechanics behind mortgage amortization — how your payment is split between principal and interest, and why early payments are mostly interest.

- mortgage amortization

- principal and interest

- how amortization works

- monthly payment

- mortgage basics

This article is for educational purposes only. It does not constitute financial or legal advice. Consult a licensed financial professional or HUD-approved housing counselor before making mortgage decisions.

Every month, millions of American homeowners make a mortgage payment — but most cannot tell you exactly what happens to that money. How much goes to interest? How much pays down principal? Why does the balance seem to barely move in the first few years?

The answers lie in amortization, and understanding the mechanics can change how you think about your mortgage, extra payments, and the true cost of borrowing.

What Is Happening Inside Each Payment

A mortgage payment is not a single charge. It is the sum of two distinct components calculated fresh every month:

- Interest — the cost of carrying your outstanding balance for one more month

- Principal — the portion that actually reduces what you owe

These two amounts always add up to the same total payment. What changes each month is the ratio between them.

The key insight: interest is calculated on your remaining balance, not on your original loan amount. As the balance drops, interest drops. Because the total payment is fixed, more of it automatically flows to principal.

The Monthly Interest Formula

For any given month, the interest portion of your payment is:

Interest = Outstanding Balance × (Annual Interest Rate ÷ 12)

That’s it. There is no magic, no hidden math. If your outstanding balance is $280,000 and your annual rate is 6.5%, you owe:

$280,000 × (0.065 ÷ 12) = $280,000 × 0.005417 = $1,516.67 in interest that month

The rest of your payment — after that $1,516.67 — reduces your principal balance.

The Amortization Formula: Where Your Payment Amount Comes From

Your fixed monthly payment is set at closing using the amortization formula:

M = P × [r(1+r)^n] ÷ [(1+r)^n − 1]

Where:

- M = monthly payment

- P = loan principal (amount borrowed)

- r = monthly rate = annual rate ÷ 12

- n = total number of monthly payments

This formula calculates the single payment amount that, applied consistently over n months, pays off exactly P with interest at rate r. It is the foundation of every mortgage, auto loan, and student loan payment schedule.

Example: A $350,000 Mortgage at 6.5% Over 30 Years

Note: 6.5% is used here as an illustrative example. Actual rates vary with market conditions, creditworthiness, and loan type. Check current rates with lenders or at Freddie Mac’s Primary Mortgage Market Survey.

For this loan:

- r = 0.065 ÷ 12 = 0.005417

- n = 360

- Monthly payment M ≈ $2,212.24

First 6 Months of the Amortization Schedule

| Month | Payment | Interest | Principal | Balance |

|---|---|---|---|---|

| 1 | $2,212.24 | $1,895.83 | $316.41 | $349,683.59 |

| 2 | $2,212.24 | $1,894.12 | $318.12 | $349,365.47 |

| 3 | $2,212.24 | $1,892.40 | $319.84 | $349,045.63 |

| 4 | $2,212.24 | $1,890.66 | $321.58 | $348,724.05 |

| 5 | $2,212.24 | $1,888.92 | $323.32 | $348,400.73 |

| 6 | $2,212.24 | $1,887.17 | $325.07 | $348,075.66 |

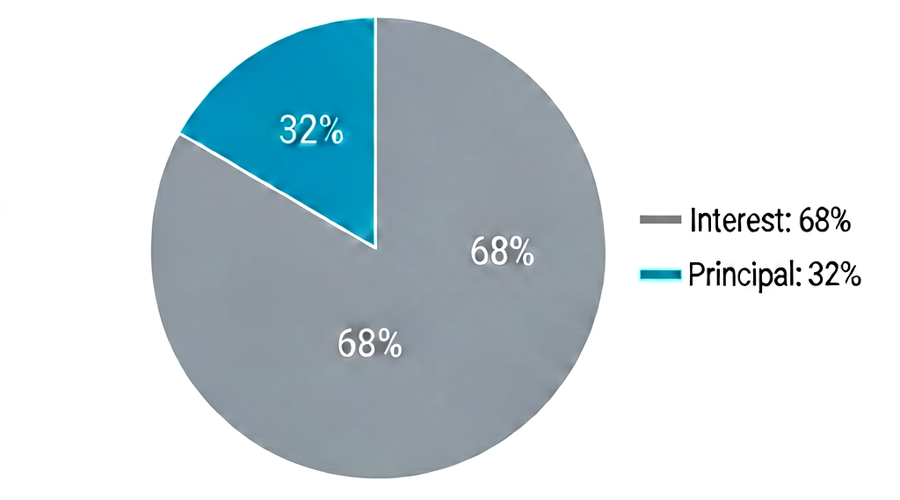

Notice that in Month 1, $1,895.83 out of $2,212.24 — about 85.7% — goes to interest. Only $316.41 reduces the balance. After six months of payments totaling $13,273.44, the outstanding balance has fallen by only $1,924.34.

This is not a lender trap. It is the direct consequence of applying the monthly interest formula to a large outstanding balance.

How the Split Shifts Over Time

The shift from interest-heavy to principal-heavy payments is gradual but relentless. Freddie Mac notes that this front-loading of interest is a fundamental characteristic of fully amortizing mortgage loans.

Here is a snapshot of how the same $350,000 / 6.5% / 30-year loan breaks down at different points:

| Year | Approx. Monthly Interest | Approx. Monthly Principal | Approx. Balance |

|---|---|---|---|

| 1 | ~$1,890 | ~$322 | ~$346,100 |

| 5 | ~$1,828 | ~$384 | ~$337,400 |

| 10 | ~$1,729 | ~$483 | ~$319,000 |

| 15 | ~$1,589 | ~$623 | ~$293,100 |

| 20 | ~$1,389 | ~$823 | ~$256,400 |

| 25 | ~$1,101 | ~$1,111 | ~$203,100 |

| 30 | ~$12 | ~$2,200 | ~$0 |

Figures are approximate and rounded for illustration.

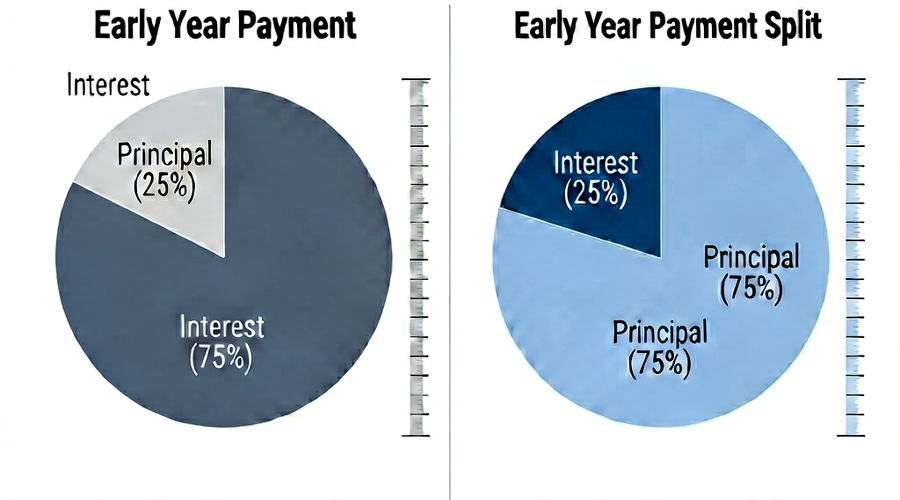

The crossover point — where principal exceeds interest in a single payment — occurs around Year 21 on a 30-year, 6.5% mortgage. Before that point, more than half of every dollar you pay is interest.

Why Early Payoff Behavior Matters

Understanding the mechanics clarifies one of the most powerful concepts in personal finance: extra payments made early save far more than extra payments made late.

Because interest is calculated on the outstanding balance, reducing the balance early means every subsequent month accrues less interest. An extra $200 in Year 1 eliminates approximately $200 of balance, which then avoids accumulating interest for the remaining 29 years. The same $200 extra in Year 25 only avoids 5 years of interest.

The compounding logic works in reverse against you when you owe money: high balances generate high interest charges. Every dollar you pay toward principal is a dollar that will never generate another interest charge.

Use our amortization calculator to see exactly how extra payments affect your specific loan — including total interest saved and months removed from your term.

The CFPB’s Perspective on Mortgage Payment Structures

The Consumer Financial Protection Bureau recommends that borrowers understand how their monthly payment breaks down between principal and interest before taking on a mortgage. For fixed-rate mortgages, the CFPB notes that the monthly payment remains constant throughout the loan term, but the proportion allocated to interest decreases each month. (CFPB — How does a fixed-rate mortgage loan work?)

For adjustable-rate mortgages (ARMs), the monthly payment itself can change when the rate adjusts, which also recalculates the amortization schedule for the remaining term.

Interest-Only Periods and Their Consequences

Some loan products — particularly certain ARMs and jumbo mortgages — have offered interest-only periods, typically 5 to 10 years, during which the borrower pays only interest and the principal balance does not decrease at all.

After the interest-only period ends, the remaining balance must fully amortize over the remaining term. This causes a significant increase in monthly payments — sometimes referred to as “payment shock” — because the same principal now amortizes over fewer years.

Fannie Mae’s guidelines for conventional mortgages that it purchases do not permit negative amortization and have strict requirements around fully amortizing structures to protect both borrowers and the secondary mortgage market.

What This Means for Your Loan Decision

When comparing two loan offers, looking at the monthly payment alone is insufficient. Two loans with identical monthly payments can have very different total interest costs, equity buildup timelines, and payoff dates depending on their terms and rates.

The amortization schedule — which you can generate in seconds with our amortization calculator — shows you the complete picture: every month, every payment, every balance, for the full life of the loan. That is the information you need to make a genuinely informed borrowing decision.

Related reading

-

15-Year vs. 30-Year Mortgage: Amortization Differences and Trade-offs

15-year and 30-year mortgages amortize very differently. Compare total interest, monthly payments, equity buildup, and which term fits different financial situations.

-

Interest vs. Principal: Why You Pay So Much Interest at the Start of a Mortgage

In the early years of a mortgage, most of each payment is interest. Understand why this happens, how the split shifts over time, and what it means for your finances.